Recent surges in the price of gold, paired with difficulty in the stock marketing following the financial collapse of 2008 have prompted many to jump onto the bandwagon of commodity investing. The logic behind this move is difficult to deny. The government is in the midst of sustained, profligate spending that does not appear to have an end in sight. This spending is going to produce increasingly high deficits as government regulation crushes private industry and innovation. When the debt burden grows too high, the government will be forced to inflate the currency as a means of financing its spending. Whenever inflation occurs, commodities are frequently the greatest beneficiaries.

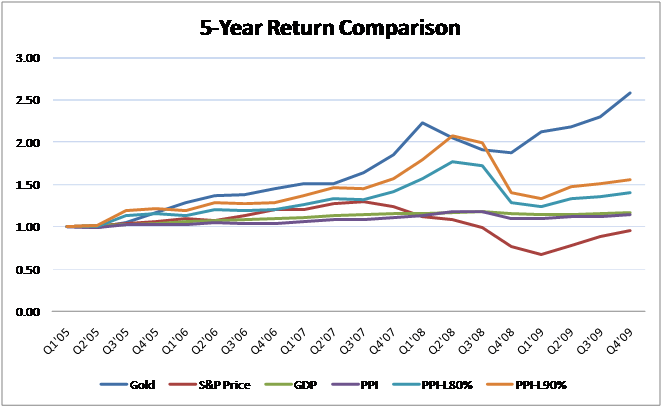

Charting out the price of gold, the S&P 500 stock index, US GDP, the Producer Price Index for all commodities, and an 80% / 90% leveraged PPI for five years seems to validate these points. The price of gold is frequently seen as an indicator of future inflation expectations, and has rocketed upward since the financial collapse of 2008. The ‘all commodities’ Producer Price Index registered a decline after the same financial collapse, due to the deleveraging of commodity portfolios by hedge funds. When this is leveraged, it extends out to compress returns such that gold vastly outperforms all of the other major indicators.

Charting out the price of gold, the S&P 500 stock index, US GDP, the Producer Price Index for all commodities, and an 80% / 90% leveraged PPI for five years seems to validate these points. The price of gold is frequently seen as an indicator of future inflation expectations, and has rocketed upward since the financial collapse of 2008. The ‘all commodities’ Producer Price Index registered a decline after the same financial collapse, due to the deleveraging of commodity portfolios by hedge funds. When this is leveraged, it extends out to compress returns such that gold vastly outperforms all of the other major indicators.

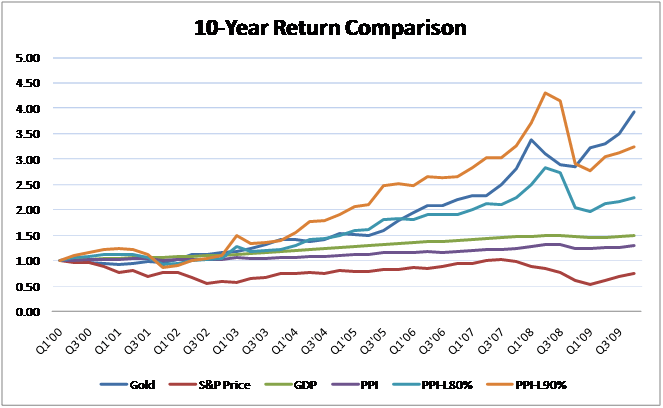

When the time horizon is extended out to 10-years, it creates a more insightful effect as the time horizon increases. By comparing the decade beginning in the year 2000, this chart effectively shows the longer term fallout from the technology bubble. The S&P 500 has not yet returned to its year 2000 value, and contracted significantly in 2008, and ended 2009 approximately 25% below its all-time high. Analysis of GDP and the Producer Price Index shows that a longer-term trend where nominal GDP compounds at a slightly higher rate than the Producer Price Index for all commodities, reflecting a slight degree of real GDP expansion above and beyond that of the indexed commodities.

The compounded rate of growth for the Producer Price Index for finished goods (not shown) is slightly lower than for all commodities and the Consumer Price Index is even lower than for finished goods. This demonstrates the impact that technology has in mitigating the impact of commodity inflation on consumers. By indexing against the PPI for commodities, it helps to control for the hedonic adjustments implicit in the consumer price index when measuring inflation.

The compounded rate of growth for the Producer Price Index for finished goods (not shown) is slightly lower than for all commodities and the Consumer Price Index is even lower than for finished goods. This demonstrates the impact that technology has in mitigating the impact of commodity inflation on consumers. By indexing against the PPI for commodities, it helps to control for the hedonic adjustments implicit in the consumer price index when measuring inflation.

If an investor leverages the PPI commodity index through the purchase of packaged commodities through income property investing, the results become quite interesting. As the amount of leverage increases, it drives a corresponding increase in the compounded growth rates for the commodity assets. However, when the PPI contracted following the financial crisis of 2008, the leveraged portfolios experienced a much greater contraction, demonstrated the double-sided impact of leverage.

The most interesting part of this extended chart is the spike of gold prices following the financial crisis. Gold prices have historically been an indicator of investor sentiment in regards to future inflation. The current price spike indicates that investors are losing faith in the ability of the US government to satisfy its debt obligations without monetary expansion. This fear has rocketed gold returns higher than even leveraged commodities in the ten years since the technology bubble’s apex.

Extending the horizon of analysis to 15 years paints a dramatically different picture. The principal reason for this is because it stretches the analysis to a point of measurement before the technology bubble had fully inflated, giving a more holistic view of the longer-term prospects of each asset class. Analysis of the S&P 500 over this extended time horizon shows a much different picture as equity values expanded dramatically during the technology bubble, crashed prodigiously, resumed expansion during the credit bubble, and crashed again. A moderate recovery in 2009 has prompted a compounded growth rate for the S&P 500 that slightly exceeds GDP (without dividends).

Extending the horizon of analysis to 15 years paints a dramatically different picture. The principal reason for this is because it stretches the analysis to a point of measurement before the technology bubble had fully inflated, giving a more holistic view of the longer-term prospects of each asset class. Analysis of the S&P 500 over this extended time horizon shows a much different picture as equity values expanded dramatically during the technology bubble, crashed prodigiously, resumed expansion during the credit bubble, and crashed again. A moderate recovery in 2009 has prompted a compounded growth rate for the S&P 500 that slightly exceeds GDP (without dividends).

This provides a very useful insight for aspiring long-term stock investors that are looking to capture high compounded growth rates as they accumulate assets for retirement. The assets of the stock market represent claims on real economic output that is articulated by the market price of financial securities. The influx of capital into the stock market over the last 25 years have led many to believe it will continue growing at past rates indefinitely. However, consider that the growth rate of real goods and services as articulated by GDP is significantly lower than the growth rate for stocks, due to the relative imbalance of people who have been buying vs. selling. As more people move out of the financial markets and seek to reap the rewards of their investing, it will result in a regression of stock market growth rates back toward the rate of real output.

Over this extended timeline, gold experiences a significant, but far less impressive compounded rate of growth. This stems from the fact that gold represents a speculative hedging instrument and not a stake in an active business entity. Since gold does not produce profits or dividends and cannot be systematically purchased with leverage, it fully depends on continued appreciation from speculators to drive rates of return.

In contrast to the speculative values of gold are leveraged commodities from the Producer Price Index. By leveraging packaged commodities over an extended period of time, it allows investors to steadily compound their asset value through increases in nominal prices that are driven by inflation. This represents a much more reliable strategy for building wealth than speculative ventures such as the stock market or gold. The reason for this is because both stocks and gold rely on a terminal imbalance of buyers relative to sellers for their values to exceed GDP.

By leveraging packaged commodities through prudent income property investments, it results in an investment product that amplifies the natural impact of inflation and protects the investor by producing cash flow that pays for the mortgage used to finance the investment property. In the short-term, there will always be popular investment fads that produce returns vastly exceeding that of leveraged inflation. However, the fortunes of these popular investments always regress back to their fundamentals as the time horizon increases. Wealth building through popular investments requires constantly timing the market to avoid the inevitable price adjustments that destroy past gains. Wealth building through leveraged investment in packaged commodities requires patience and perseverance to wait for the right opportunity before buying or selling. If given a choice between trying to outsmart the market every year and patiently waiting for the right opportunity to buying and sell packaged commodities through leveraged income property investment, I will always choose the patient prudence of leveraged commodities over the fast frenzy of market timing.